It’s The Economy Stupid!

Capital & Interests:- What is the plan for Britain’s much maligned housing market?

As the dust settled on Labour’s landslide victory, talking heads across the UK began the inevitable task of predicting what the government may spend their initial political capital on. Having won a wide but thin mandate on a manifesto of caution and limited ambition, would they choose this moment to jolt the electorate with a series of bold but controversial policies? Yes & No.

Capital & Interests:- What is the plan for Britain’s much maligned housing market?

As the dust settled on Labour’s landslide victory, talking heads across the UK began the inevitable task of predicting what the government may spend their initial political capital on. Having won a wide but thin mandate on a manifesto of caution and limited ambition, would they choose this moment to jolt the electorate with a series of bold but controversial policies? Yes & No.

Down with the Nimbys

Planning reform doesn’t send anyone’s heart (even mine) racing but hidden behind the veil of the image of a clipboard wielding planning officer turning down your request for a larger side return, lies a fundamental shift in how the country could look and feel in 50 years’ time. Ripping up red tape is supposed to be a line from the Tory playbook, however allowing for houses to be built on “greybelt” land and alongside the return of mandated targets and newly imbued powers for Metro Mayors, means at least more houses may well get built in this parliament than did in the last.

This policy should be no surprise to anyone who read the Labour manifesto, but did many understand what it really meant? While many cry out for more homes when asked on a generalised survey, when faced with the prospect of it happening near their home, many are actually against more homes being built, let alone wind farms or train lines. Improved infrastructure has the power to link communities and bring wealth and prosperity to areas of the country that modern Britain has left behind, however many will bemoan more hard hats and cranes coming to a town near you.

Chaos under Rishi Sunak, strong & stable with Starmer?

Building a good house requires strong foundations, reliable financing and a builder you can trust. Rachel Reeves (congratulations to the first female Chancellor EVER), spent the last 2 years showcasing her credentials as a safe pair of hands and a steward of economic stability. In part the Labour party also have currently high mortgage rates to thank for their election victory, especially in the large swathes of the now crumbled blue wall. With Labour making house building a key plank of their policy platform, house builders will need confidence that young buyers will be there to actually buy these homes. This means keeping interest rates at a level where borrowers can afford to borrow. Reeves spent a good portion of her career working at the Bank of England and while she has no direct control of monetary policy she will be looking for an accommodative rate environment to help with their central growth agenda. Will Andrew Bailey and Co play ball? They will be at pains to de-politicise the bank and ‘follow the numbers' and with no growth targets within their own mandates, as long as inflation remains a threat they may keep their own powder dry longer than the government may like. However with rates already forecast to fall over the coming 12 months, the new government may have timed their coming to power to economic perfection.

What about Tax?

I have already written about the scale of inequality within the UK housing market. As economist and new Labour MP Torsten Bell writes in his new book “Great Britain?”, two ways of making sure you get on in the UK’s bonkers housing market are choosing your parents or your partner carefully. With the government making clear not to raise taxes on “working people” are they leaving the door open to other property or wealth related taxes? Re–banding council tax bands remains a rumour. What impact would this have on the value of high-end London homes and would this be tantamount to the much feared “mansion tax” touted by Ed Miliband? However, for those of you concerned about the enormous divide between the haves and the have nots, can the housing market continue to grow on the back of untaxed wealth moving from generation to generation with little to no controls?

We are a business with a sincere interest in the financial wellbeing and success of our clients and customers. We wish this government, as we would any government all success. It is important to remember, all of us are and should be on Team UK.

Mortgage Capacity Assessment Reports & Expert Financial Guidance

Divorce is an incredibly stressful and emotional experience. To achieve the best outcomes, it's important for various professionals to collaborate and offer support. We have extensive experience in producing mortgage capacity reports for use in divorce proceedings. We understand what information is relevant to the decision-making process and how to handle this sensitive topic.

Divorce is an incredibly stressful and emotional experience. To achieve the best outcomes, it's important for various professionals to collaborate and offer support.

We have extensive experience in producing mortgage capacity reports for use in divorce proceedings. We understand what information is relevant to the decision-making process and how to handle this sensitive topic.

The mortgage capacity report is intended for you and your trusted advisers to demonstrate mortgage borrowing capacity, facilitating a fair division of assets. We take the time to thoroughly discuss all details with our clients, their solicitors, and their financial advisers to ensure our assessment is fair and accurate.

From April 2022, mortgage capacity reports became mandatory for all court cases. We completely overhauled our process and the structure of our report, working with family solicitors and financial advisers to ensure that the content was relevant and concise in all cases.

When it comes to the mortgage capacity report, we must be unbiased and provide a fair assessment of mortgage borrowing. This may include multiple scenarios, or there may be no mortgage capacity at all.

We regularly work with Evelyn & Partners and their Family Team. We interviewed Lucie Spence, Partner and Director of Financial Planning at Evelyn & Partners, and asked her some questions about the topic and why the reports are important. This collaboration shows how our advice and theirs are closely connected and how we support each other in delivering excellent customer outcomes when they are most needed.

-How does a mortgage capacity assessment assist with wider financial advice in the divorce process?

Lucie: It can support the wider conversation around how much an individual would need to deposit to buy the home they are considering. It also supports the conversation around what type of house an individual can afford to purchase and the potential running costs of this property. When supporting lawyers with agreeing on a financial settlement, we go through a cashflow plan with our clients and we factor into this the level of expected borrowing and the potential interest rates to show whether this is affordable for clients. Also, it supports financial advisers in advising on a split between borrowing and investing and the right balance between the two. Should an individual wish to buy out their ex-partner from the marital home we can show the financial implications of this both in the short and longer term.

Jess: When going through a divorce, it's important to consider various outcomes. Factors such as the amount of deposit available, potential child or spousal maintenance, and cash flow planning are crucial. If one party wants to buy out the other from the family home, we can include this in the report to ensure affordability. Our reports can present different scenarios alongside cash flow analysis to illustrate the overall financial picture for the client. This helps in understanding how a mortgage loan will impact the individual both now and in the future, allowing for a fair division of assets to be agreed upon.

-What wider financial planning objectives do you consider for clients going through a divorce?

Lucie: Cash Flow planning should demonstrate how the settlement could be used to provide income or lump sums now and in the future. It also supports showing the settlement's value for the individual in terms of how long it will last at their proposed rate of spending. Financial education is vitally important for clients, and this is one of the foundations of the advice we provide. Many clients I work with have never managed their finances, so we start by talking them through the basics. Protection to cover maintenance and children costs and to replace what has potentially been lost through the divorce. Many clients have their spouses covered through their work benefits in terms of life cover, income protection or critical illness, but this is then lost when the divorce goes through Pension provision to ensure clients are making the most of their pension contributions Child Benefit ensures that the right party is claiming this benefit to ensure national insurance credits are continued. Loan repayments where possible to try and support clients to start the new chapter of their lives Investment advice, either advising on existing investments and ensuring they are structured in the right way or advising on a new cash lump sum which may have been received as a result of the divorce due to pension offsetting or a capitalised maintenance lump sum Implementing pension sharing orders which have been agreed through the court. We also have defined benefit transfer specialists who can advise when a sharing order is placed on a Defined Benefit scheme. Should the individual own a business we can provide support and advice around their options so that informed decisions can be made. Provision for children’s education

Jess: All of these broader financial planning goals will influence how we assess mortgage capacity. Factors such as education expenses, investments, and other sources of income will all affect an individual's borrowing potential. It is essential for us to comprehend how these factors will impact future mortgage capacity assessments.

-What other essential advice can you offer clients who are going through divorce and how do you help and support them in the aftermath?

Lucie: Untangling finances during a divorce can be emotional, and decisions that are made can have a long-lasting impact. Often, individuals effectively ‘pay off’ their other half just to move on with their lives and then regret this decision later when the implications become apparent. Engaging with clients as a financial adviser early on can support them in not making knee-jerk emotional financial decisions. For some clients, this may be the first time that they have managed their money and have a lack of understanding around investments or pensions. This is where we can really support financial education and the explanation going forward. We can also support the tax position when the assets are split, and the spousal exemption applies. We would also support clients going forward with their new lives and work with them to adapt their financial plans when their circumstances change. Generally, our clients have a long-term relationship with us as their financial advisers (many of mine have worked with me for over 20 years) and will meet with us at least on an annual basis, and we become their trusted advisers, often going on to advise their children.

Jess: The first time people inquire about how much they can borrow for a mortgage can be a new experience for them. For us, it's not just about creating a report for the court but also providing support afterwards. We prepare reports indicating that there is no mortgage capacity at all, which can be surprising for some people. Therefore, it's important for us to support and educate them, explaining how and why we reached our conclusions so they can move forward confidently and with understanding.

-How can this information prove valuable in negotiating a divorce settlement's property division, spousal support, and other financial aspects?

Lucie: Working with legal professionals & using the mortgage capacity report to understand how much an individual can afford to buy a new property and ensure that they have enough income or capital to fund their lifestyle going forward is an important part of the process. We can also help to discuss with the client whether or not this is realistic over the longer term or whether they need to have a larger settlement, borrow less or reduce their outgoings. Should an individual receive a capital lump sum instead of ongoing maintenance, we can calculate the capital amount depending on the client's risk level. We also work with clients' legal representatives to determine how much income can be generated from varying lump sums. We explain the value of money to individuals and evidence how much disposable income they would have depending on the mortgage level they take out and the impact of rising or falling interest rates. This can then support the clients and legal professionals with the negotiation, and we can run the calculations required depending on their requirements. It also shows where suggested settlements are not affordable to an individual and the impact on them in later years. For example, when an individual keeps a marital home but doesn’t have any pension provisions, we can work with them to understand the changes that will need to occur in their later years to afford their retirement.

Jess: The first part of the report emphasises the importance of taking into account various aspects when undergoing a divorce. It underscores the significance of professionals working together to provide the required information for a fair evaluation of the situation and the division of assets.

We are committed to providing personalised, compassionate customer service at the heart of everything we do at Anderson Harris. Divorce is a challenging time for everyone involved, and we strive to offer necessary support in a timely and sensitive manner. Many of our clients initially approached us for a mortgage capacity report and have since become long-term clients. We also collaborate with their other professional advisers. If you would like to discuss any of the topics mentioned in this blog, please reach out to us. We are more than happy to assist in any way we can, including providing referrals to relevant services.

Beyond Avocado Toast

In the UK, our home is our castle, and this cornerstone of British life is in many ways our unique obsession. But if home ownership is so popular, economically beneficial, and politically supported, why has it become so difficult for those who do not own a home to go out and buy one? In chapter two of our Capital and Interests series we ask what we have to do to be considered worthy of home ownership?

Capital & Interests: The Changing Face of the UK Mortgage Scene

Harry Arnold 04 06 2024

a tasty problem

In the UK our home is our castle, and this cornerstone of British life is in many ways our unique obsession. But if home ownership is so popular, economically beneficial, and politically supported, why has it become so difficult for those who do not own a home to go out and buy one? In chapter two of our Capital & Interests series we ask what we have to do to be considered worthy of home ownership and what are the growing number of innovations in the mortgage market that have arrived on the scene to help more of us get there?

Cancelling your Netflix subscription and cutting back on avocado toast probably won’t do it, despite this song being sung at those under the age of 40 for some time now. The truth is that those unable to draw on significant support from their family, or those without abnormally high salaries, are being priced out in a market that exemplifies the economics of “the haves and have nots”.

The UK property market, worth an estimated eight-trillion pounds, holds a significant portion of the country’s wealth. The people holding that wealth have little desire to give it up, and any political party that suggests they might is swiftly told by the electorate to please think again. The old economic battleground of Baby Boomers vs Millennials is beginning to give way to an even more nuanced confrontation: Millennials with an inheritance, and Millennials without.

So, what’s being done to level the playing field? It’s probably going to take an extended period of fundamental reform to help the UK escape stagnation and enter an age of equality and prosperity, where our wages increase above the rate of house price inflation, and peace and love is extended to all. In the meantime, innovation in the mortgage market will have to do.

Luckily, help is at hand, thanks to a growing family of products designed to help Generation My-Landlord-Is-Upping-My-Rent. From Ultra Long Mortgage Terms to trendy Scandi style loans, a new generation of mortgage products is hitting the market.

What is new on the shelves?

The Track Record Mortgage hit the shops from Skipton Building Society in May 2023. It’s a simple option, allowing for a 100% mortgage with no deposit, as long as your mortgage payment is no higher than the rent you currently pay. When making a credit decision, this option takes into account your performance as a renter, which is fairly unique amongst retail lenders. You’ll still need to adhere to Skipton’s strict lending criteria, have a picture perfect credit rating and if you’re living at Mum and Dad’s, this one isn’t for you.

The 5k Deposit Mortgage is the most recent offering from Accord Mortgages, only launched a couple of months ago. This option allows for someone to borrow with a minimum £5k, or 1% deposit, on a maximum purchase price of £500,000. No flats allowed, and an immaculate credit score is required. This option is great for anyone who’s saved up some money by moving back in with Mum and Dad, but also have a quality job to lean on, driving affordability for the mortgage itself.

The thing that sets these two apart from the more traditional Joint Borrower Sole Proprietor offered by several larger banks, is that they are focused on the worthiness of the individual, rather than relying on parents participating in the mortgage, or putting their money on deposit with the bank - as we see with the Family Springboard Loan offered by Barclays. An honourable mention also to the Dutch, with newcomers April Mortgages and Perenna bringing Long Term Fixed Rate options that may well be a superb option for those who want to go big on the borrowing with no exposure to the rate market.

Although it’s exciting to see these products coming out, offering innovative solutions - it’s important to note that they are provided by small institutions. They’re not currently being offered by the big banks with their big boy balance sheets - and until they start to get on board, the dial is unlikely to shift dramatically.

how we can help

It’s a long road to a more accessible housing market, but these innovative products offer stepping stones for aspiring homeowners. Perhaps, with continued innovation and a focus on individual merit, the dream of homeownership could become a reality for a wider segment of the population.

Navigating these choppy waters is challenging, and as always advice is critical when you’re seeking any mortgage, especially if you’re diving in for the first time. Reach out for a conversation with a member of our team today.

The Parent Trap

Last month’s widely publicised rollout of the government’s ‘free childcare’ offering contains a clause that many hard-working families are likely to find frustrating and disappointing, given the considerable financial strain the cost of childcare puts them under; the exclusion of any and all support if one parent earns over £100,000. No tax-free childcare, and no free hours until the child reaches 3.

Capital & Interests: The creation of the ultimate frozen threshold.

Harry Arnold 14 05 2024

WHAT is going on?

My wife works in public policy, and I’ve learnt to look forward to her nightly report, in which she offers me some insight into the way various government sausages are made. It appears creating policies that make everyone happy is either impossible, highly implausible - or completely unaffordable. In this first instalment of Capital & Interests, it’s the subject of affordability that I’d like to shine a light on.

Last month’s widely publicised rollout of the government’s ‘free childcare’ offering contains a clause that many hard-working families are likely to find frustrating and disappointing, given the considerable financial strain the cost of childcare puts them under; the exclusion of any and all support if one parent earns over £100,000. No tax-free childcare, and no free hours until the child reaches 3.

£100,000 is a large annual income, and perhaps you’re of the belief that it’s not the responsibility of the taxpayer to support the richest among us. But although £100,000 sounds like a lot of money, let’s consider it within the context of a London housing market gone mad, where people are expected to find half-a-million to buy a garden flat with rising damp and poor transport links . £100,000 just isn’t what it used to be.

This is especially true if you don’t count yourself among the growing number of millennials inheriting baby boomer wealth. These days, this cohort could be looking down the barrel of a fairly large mortgage, in an elevated interest rate environment, to buy a pretty standard house south of Watford. For a generation born into the “End of History”, who have likely followed the New Labour path through university in order to secure a “high paying job of the future”, this is a fairly bitter pill to swallow. Let’s not forget their student loan payments, currently sitting at 7.8% for a plan 2 loan.

HISTORY

It was the late Alastair Darling - as I write this, the last Labour Chancellor - who introduced the £100,000 threshold in 2009, when it was decreed that anyone earning over this sum would start being denied a personal allowance, thus creating the dreaded 60% tax rate and it has not moved an inch since. According to Nationwide’s House Price Calculator, in the fifteen years that have passed since this decision, house prices in London have risen by 102% and according to the Bank of England’s own Inflation Calculator, goods and services that would have cost you £100,000 in 2009 will now cost you £153,670. This is the ultimate frozen threshold.

the effect

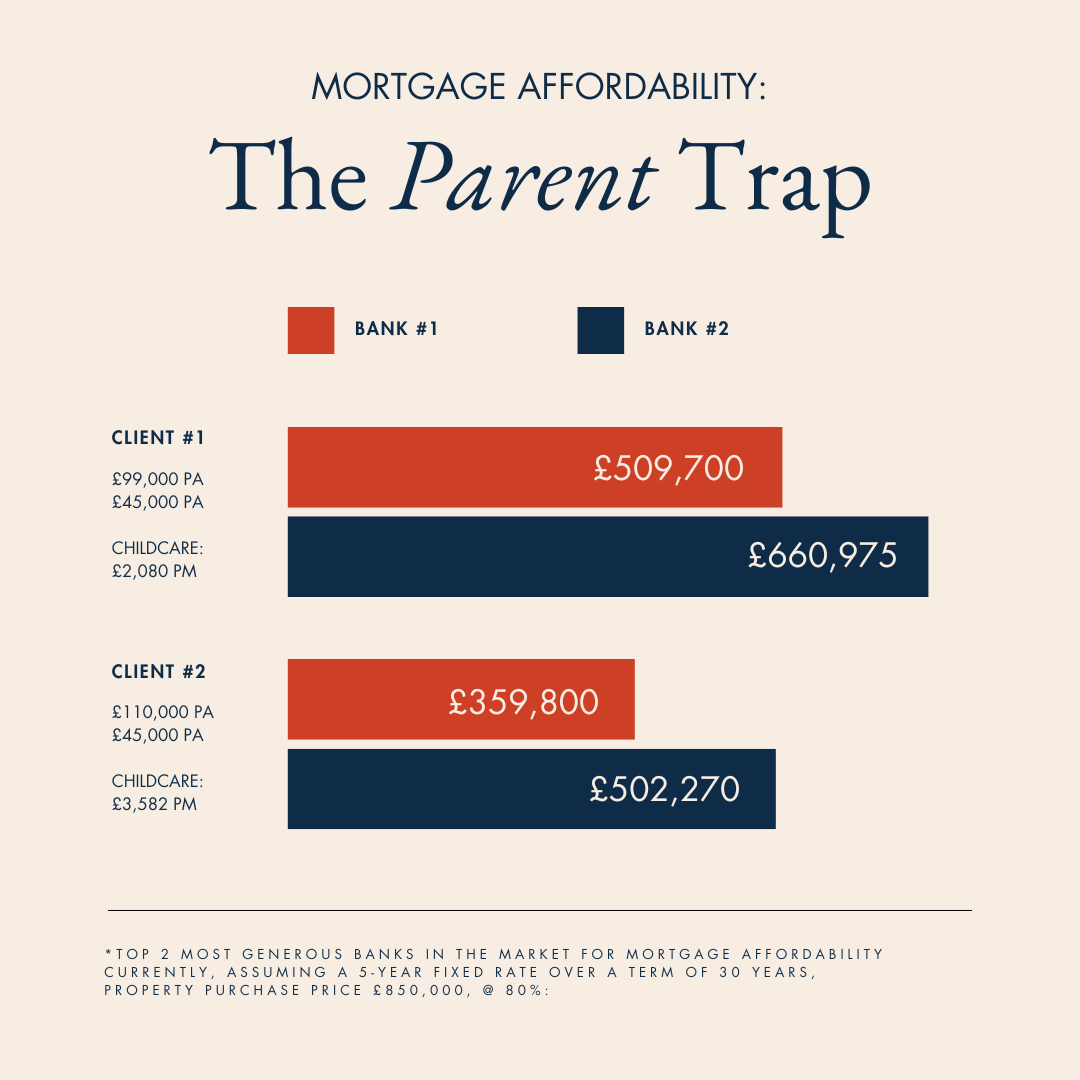

After an internal analysis of the two banks who currently have the most generous affordability calculations on the high street, we also found that this removal of support has a profound impact on mortgage affordability for higher earners. If you’re receiving no government support, an example cost of full-time nursery based in a South London borough (mine, actually) for two children under the age of three comes in at £3,528 per month.

For a partner of someone exceeding the £100,000 threshold, assuming they make a 5% pension contribution and have a plan 2 student loan, this £3,528 figure is the rough equivalent of the net monthly salary of £64,000 per annum. The uncomfortable reality is that unless the second earner exceeds this level of salary, there’s little point in them working and the family committing to these childcare costs. Another striking point with regards to mortgage affordability is that in our model, only when someone is earning £145,000 and not receiving the benefits would they be able to borrow more than someone earning £99,000 and receiving their full childcare benefits. That’s a 46% gap.

This is a metropolitan problem, yes - but it’s one being faced by the people in our society that we hold up as aspirational role models. Hard-working families, making it on their own with little to no parental support. High-earners who have worked their way up to a “high paying job of the future”, and, with house prices where they are, significant mortgages.

how we can help

As we navigate the market, it’s increasingly obvious that generic solutions rarely meet specific needs. At Anderson Harris, we understand unique circumstances, and we’re committed to providing bespoke financial solutions that align with your needs. Whether you’re grappling with the challenges of mortgage affordability, or seeking strategic advice on how to manage your finances amidst new policy changes, our team is here to guide you.

Reach out for a conversation with one of our advisors today, so we can explore the options available, and discuss how we can tailor our services to support you.

Your Journey Home Starts Here

Discover how we at Anderson Harris simplify your mortgage journey with expert guidance and personalised service. Our revamped approach ensures a stress-free experience, letting you focus on the joys of home ownership. Explore our bespoke solutions today.

At Anderson Harris our approach to client service is simple yet impactful: from the initial consultation to the successful securing of their mortgage and beyond, we ensure a smooth, understandable, and bespoke experience tailored for every individual. Our goal is a stress free process for the time poor, where our clients can focus on the joys of home ownership, while we take care of the financial essentials.

A fresh look, same approach

While our focus remains fixed on the ongoing financial success of our clients, after thirteen years in the market we felt it was time for a refresh of our brand, making sure that how we look and feel, reflects the standards we set ourselves in delivering for borrowers every day. We also want to take this opportunity to reaffirm to you, our clients and counterparties, that our core values of competence, transparency and decency remain the cornerstone of our offering to the market. Our rebrand marks the start of a new chapter for our firm. With your support, we feel it is time for our offering to reach more people, so more of them can get the award winning, highly respected advice that so many of you and your clients already experience.

What to expect from us?

What is required to be an advisor in the digital world of 2024? With so much swirling information around mortgages and its place in our economy, our enhanced digital offering will be a calming tonic to the noise. With a new generation of borrowers looking to seek guidance online, expect to see more client-centric insights, explainers & tips from us across multiple platforms, so that more borrowers can access the quality advice they deserve. We will be there as a regulated, professional voice, talking about topics that relate to our clients financial lives and requirements, nothing else.

Our Rebrand Reflects Our Commitment to You

Our recent rebranding is a reflection of our commitment to being by the side of every client throughout their mortgage journey, not only from transaction to transaction, but also as an ongoing source of useful, relevant mortgage news and editorial commentary. The new look and feel encapsulates our ethos of clarity, trust, and personal guidance.

The journey, together

Choosing Anderson Harris means choosing a partner whose determination to succeed mirrors the home ownership dreams of our clients. Take a look at our process, and send us an email to learn more about how we can help you navigate paths to homeownership with ease and confidence.

Call us today on 020 7495 6633 or email enquiries@andersonharris.co.uk.